For most IRA Millionaire households, a Roth conversion is no longer an unfamiliar concept. The strategy makes sense. The reasoning is clear. There’s a part of you that already knows it should be in motion. But there’s also a part that’s been telling yourself you’ll get serious about it later — at year-end, after the markets settle, after the next conversation with your CPA, after your spouse is fully on board, after things feel a little more certain.

Those reasons aren’t crazy. They’re actually pretty logical, and after more than 14 years of building conversion plans for 2,400+ IRA Millionaire households, our team has heard every one of them. The problem is that waiting carries a specific price tag, and most households have never seen the number. This article walks through what a year of delay actually costs — pulled from real conversion plans, not hypothetical examples — what five years of delay costs, and why the math of compounding now works against the household rather than for it.

The Reasons People Wait (And Why They Sound Reasonable)

Most households have several legitimate-feeling reasons to push a conversion decision into next year. The most common patterns our team hears:

- Markets feel uncertain. Volatility makes any major financial move feel premature.

- Account complexity. Households with traditional IRAs at multiple custodians, plus 401(k)s, plus inherited IRAs, sometimes feel paralyzed about which accounts to touch first.

- CPA bandwidth. Many households want to coordinate with their CPA, but tax season just ended and bothering them feels rude.

- Spouse alignment. One spouse is fully on board; the other is still warming up to the idea.

- The “wait until things settle” instinct. A general sense that the household should wait for a clearer moment before pulling the trigger.

None of these reasons are irrational. They are common, recurring, and grounded in real life. But each one quietly converts into a measurable lifetime cost — and the cost is much larger than most households expect.

Stop the Clock on Your Conversion Cost

Our team has built more than 2,400 multi-year conversion plans, and the sample plan in this article reflects patterns we see across thousands of households. Find out what waiting is actually costing your specific situation — with no product pitch and no obligation.

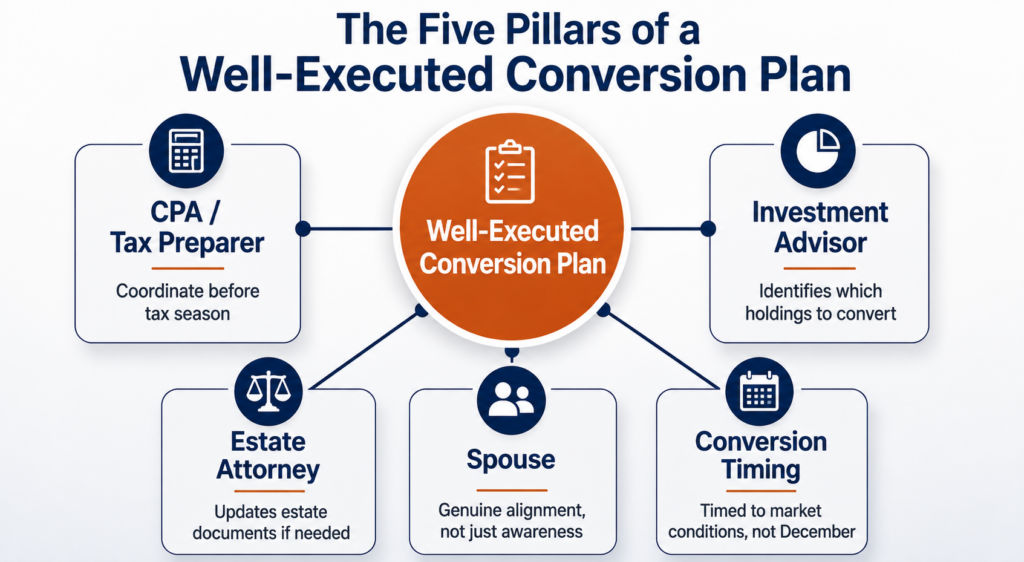

The Five Things That Make a Conversion Plan Actually Work

A well-executed Roth conversion is not a single transaction. It is the result of five separate elements coming together, each with its own lead time.

Your CPA or tax preparer. Tax season runs February through April. To coordinate estimated payments, withholding amounts, and conversion timing properly, the CPA needs to be in the loop before they’re buried in filings. Miss the window and the coordination conversation gets pushed to next year.

Your investment advisor. The question isn’t only how much to convert — it’s which specific holdings to convert first. Identifying the right ones takes real evaluation across the portfolio. Rushing that decision into the last few weeks of December rarely produces the optimal sequence.

Your estate attorney. Converting changes the tax character of assets from pre-tax to tax-free. That shift can affect how inherited accounts pass to heirs. Existing estate documents may need updates the household didn’t anticipate.

Your spouse. This strategy affects both spouses, including what happens to the surviving spouse if one passes first. The sooner both spouses are fully in the picture — not just aware, but genuinely part of the decision — the more confidently the plan gets executed.

Conversion timing within the year. The right moment to convert isn’t automatically December. It’s when market conditions and tax positioning actually align. That opportunity only exists when the household has more of the year remaining, not less. By December the window is largely closed.

Why Compressing the Year Compresses Execution, Not the Plan

Households often assume a late start just means working faster. The plan itself can still be built well — the math, the projections, the sequencing all still work. What gets compressed is something different: the execution window.

The plan is not where the value lives. Execution is. A plan sitting in a folder doesn’t reduce a household’s lifetime tax bill. The conversion sequence, the timing, the coordination across CPA and advisor and spouse — the actual implementation — is what generates the dollar outcome.

Our team’s research across thousands of conversion plans shows that conversions executed with a full planning year — proper coordination, the right timing, strategic investment selection — can add as much as $30,000 of value for every $1 million converted, compared to plans executed in the compressed last six weeks of the year. That difference isn’t created by a better plan. It’s created by everything around the plan having the time to work. For more on annual timing specifically, see our team’s analysis of the best time of year for a Roth IRA conversion.

The Real Cost of Waiting (One Year vs. Five Years)

Here’s the part that stops most households cold. The numbers below come from a real sample plan our team modeled. Specific dollar figures will differ from household to household — IRA balance, age, income, and tax-law context all vary. The direction is the same across thousands of cases.

Consider a household whose well-executed Roth conversion strategy, started now with a full planning year and proper coordination, produces approximately $1.8 million in projected lifetime tax savings. That’s the baseline — the dollar value of acting.

Now consider what waiting looks like.

| Decision | Projected Lifetime Tax Savings | Cost of Delay |

|---|---|---|

| Start now, full planning year | ~$1.8M | — |

| Wait one year | ~$1.73M | ~$66,000 |

| Wait five years | ~$1.44M | ~$357,000 |

Sit with those numbers for a moment.

$66,000 of lifetime tax benefit, gone, because the household waited one tax year. Not because the plan got worse. Not because anything went wrong. Simply because the window was one year narrower.

$357,000 of lifetime tax benefit, gone, after five years of delay. Five years of “I’ll get to it” or “I’ll handle it next year” or “I’ll wait until markets are more certain” or “I’ll wait until I’m in a lower tax bracket.” That money doesn’t disappear. It stays in the IRS’s pocket — and comes directly out of what the household, the surviving spouse, and eventually the heirs would have kept. For more on the size of optimization differences in real plans, see our team’s analysis of strategic Roth conversions that save over $1 million in taxes.

Why Compounding Now Works Against You

Most IRA Millionaire households built their wealth by understanding compounding. Every year the IRA grew, the next year’s growth happened on a larger balance, and over thirty or forty years that produced real wealth.

That same force is now working against the household. Every dollar sitting in a traditional IRA will eventually be taxed at ordinary income rates — that was the agreement made when the contribution went in. The only remaining question is when and on what amount the tax gets paid. While the household decides, the account keeps growing. Every dollar of growth is another dollar the IRS has a claim on.

The longer the balance sits in the traditional IRA, the larger the IRS’s share becomes. A statement that shows $2 million includes a meaningful portion that was never the household’s to spend. The window to actively manage that exposure is open right now. It does not stay open forever.

How to Get Your Plan Moving This Year

A useful starting point is knowing the projected size of the future RMD problem the conversion is designed to solve. Our team has built a free RMD calculator that shows exactly what a current IRA balance is projected to become at age 73, and what the IRS will require be withdrawn starting that year. The calculation takes about two minutes. Most households who run it are genuinely surprised by the number.

From there, the planning sequence is straightforward in principle:

- Quantify the future RMD picture against current income, Social Security, and pension projections

- Bring the CPA into the conversation before tax season closes the window

- Get the spouse fully aligned on the strategy, not just informed

- Loop in the estate attorney if document updates are required

- Build the multi-year conversion sequence with the investment advisor before the year compresses

For more on why multi-year planning beats single-year decisions, see our team’s analysis of multi-year Roth conversion strategies.

Common Mistakes to Avoid

Several errors quietly compound the cost of delay:

- Treating the conversion as a December transaction. A real plan needs a full year of execution runway. The last six weeks aren’t enough.

- Waiting for the CPA conversation until next tax season. The right time to coordinate is now, between filings, while the CPA has bandwidth.

- Postponing the spouse conversation. Plans stall most often because one spouse isn’t fully in the room. Getting full alignment early is more valuable than getting the math perfect later.

- Confusing “I have a plan” with “I have a result.” The plan in a folder doesn’t reduce taxes. The execution does.

- Waiting for markets to feel certain. They never feel certain. The right time is when the household’s situation supports the move, not when the headlines feel reassuring.

For a broader look at the planning errors that derail conversion strategies, see 5 costly Roth conversion mistakes.

About Q3 Advisors

Q3 Advisors is a flat-fee fiduciary firm specializing in tax-efficient retirement planning for high-income professionals and retirees. As practitioners of Rothology® — the science of Roth conversion optimization — our team brings the multi-year modeling, coordination expertise, and execution discipline that separate a conversion plan that produces real lifetime savings from one that simply sits in a folder. With $9 billion in projected tax avoidance for our clients over more than 14 years, we have the track record to guide your strategy.

Frequently Asked Questions

What is the actual cost of waiting one year on a Roth conversion?

For one sample plan our team modeled, the cost of waiting one tax year was approximately $66,000 in projected lifetime tax savings. Specific dollar amounts vary by household — IRA balance, age, income, and tax-law context all matter — but the direction is consistent: every year of delay narrows the execution window, and the lifetime cost is measurable.

Why does waiting cost so much when the plan itself doesn’t change?

The plan is the math. The value is in the execution. A full planning year provides time to coordinate with the CPA before tax season, identify the right specific investments to convert, align both spouses on the strategy, update estate documents if needed, and time conversions to actual market conditions. Compressing all of that into the last six weeks of the year shrinks the execution window — and execution is where the dollar outcome lives.

When is the best time to start a Roth conversion plan?

The first quarter offers the widest planning window. CPAs are most accessible just before and just after tax season. Markets have a full year for tactical opportunities to emerge. The conversion sequence can be calibrated month by month. December starts work but are heavily compressed and rarely produce the optimal result.

What if I’m already several years into thinking about conversions but haven’t started?

The best time to start was when the conversation first came up. The second-best time is now. Each year of additional delay carries an additional cost. The plan built today won’t perfectly match the plan that might have been built five years ago, but it will be materially better than the plan that gets built five years from today.

How does waiting interact with required minimum distributions?

Every year the traditional IRA balance grows, the eventual RMDs grow with it. RMDs are calculated as a percentage of the balance, applied annually starting at age 73 (or 75 for some later birth cohorts under SECURE 2.0). A larger balance means larger forced taxable income for the rest of retirement. Conversions completed before RMDs begin shrink that future forced-income problem.

Why is coordinating with my spouse so important?

A Roth conversion strategy affects both spouses, including what happens to the surviving spouse after the first passes. The “widow’s trap” — where single-filer brackets and IRMAA thresholds hit at much lower income levels than joint thresholds — magnifies the cost of leaving a large traditional IRA balance in place. Plans where one spouse isn’t fully aligned tend to stall, and the cost of that stall shows up in the same per-year dollar figures.

Plan Your Roth Conversion Strategy Today!

The math is simple even when the strategy isn’t. Every year of delay on a Roth conversion plan has a measurable lifetime cost — $66,000 in one sample plan after a single year, more than $350,000 after five. The plan in a folder doesn’t reduce taxes. To find out what waiting is costing your specific household — and what a fully coordinated plan looks like for your numbers — schedule a consultation with our team and get a multi-year projection built around your numbers.