The 5-year rule for Roth IRAs is one of the most consequential — and most misunderstood — pieces of retirement tax law. It governs when earnings inside a Roth can be pulled out tax-free, and a single misread of the clock can convert a “tax-free” withdrawal into a taxable distribution with penalties layered on top. For an IRA Millionaire running a multi-year conversion plan, the stakes compound: each conversion year starts its own clock, and the wrong sequence can leave six figures of Roth balance temporarily off-limits.

What follows breaks down both versions of the rule — contributions and conversions — explains exactly when each clock starts, walks through what changes after age 59½, and surfaces a counterintuitive planning move that helps IRA Millionaire households accelerate their Roth strategy without putting another dollar into a Roth contribution.

Craig Wear and his team at Q3 Advisors have built thousands of Rothology™ game plans for households with $1M+ in IRA assets — averaging more than $3 million in projected lifetime tax savings per family. The patterns below come from that body of work.

What the 5-Year Rule for Roth IRAs Actually Means

The 5-year rule is the IRS condition that determines when earnings inside a Roth IRA can be withdrawn tax-free. It is not one rule but two — one for Roth contributions and a separate one for Roth conversions. Each version uses its own clock, and the language difference matters: a contribution is money moved into a Roth from a household’s pocket. A conversion is money moved into a Roth from an existing pre-tax IRA or 401(k), with tax paid on the converted amount in the year of the conversion.

Talk With Craig Wear's Team

Craig has helped IRA millionaires save over $1 million each in unnecessary taxes. Find out if a Roth conversion strategy fits your retirement, with no sales pressure and no product pitch.

Both versions of the rule share a common purpose: they prevent the Roth from being used as a short-term tax-shelter for earnings. The IRS requires real time inside the Roth before it lets earnings come out tax-free.

The 5-Year Rule for Roth Contributions

The contribution clock starts on January 1 of the year a household makes its first Roth IRA contribution to any Roth IRA — not the date of the deposit itself. The clock applies across every Roth IRA an individual owns over a lifetime, not separately to each account.

To take tax-free withdrawals of the earnings, two conditions must be met:

- The Roth IRA must have been open for at least five tax years.

- The owner must be at least 59½, or qualify under a narrow set of exceptions (disability, first-time home purchase up to $10,000, certain medical expenses).

A simple example: a household contributing to a Roth in March 2020 starts the clock at January 1, 2020. The five-year period closes on January 1, 2025. If the owner is at least 59½ at that point, every dollar — contributions and earnings — can be withdrawn tax-free from that point forward.

The original contributions themselves are a separate matter, covered below.

The 5-Year Rule for Roth Conversions

The conversion clock works differently. Each Roth conversion starts its own five-year clock, again beginning on January 1 of the year of the conversion. A conversion completed in November 2026 starts a clock that closes on January 1, 2031.

A household running a multi-year conversion plan therefore has multiple overlapping clocks. The 2026 conversion has one five-year window. The 2027 conversion has its own. The 2028 conversion starts fresh again. Each tranche of converted dollars carries its own holding requirement before the earnings on that tranche can be withdrawn without penalty.

To withdraw converted amounts free of tax and penalties, the household must wait five years from the conversion year, and the owner must be 59½ or meet one of the qualifying exceptions.

When the Clock Actually Starts

The IRS treats both 5-year clocks as starting January 1 of the relevant tax year, regardless of when during that year the contribution or conversion actually occurred. The practical effect: a November conversion gets credit for almost 11 months of clock time that hadn’t actually elapsed yet.

For an IRA Millionaire running a multi-year plan, this is a real planning lever. A conversion completed before December 31 captures an extra year of clock time compared to the same conversion completed two weeks later.

What Past 59½ Means for the Conversion Clock

One of the most consistently misunderstood points: once a household is past 59½, the 5-year rule on conversions only applies to the earnings on those conversions, not the converted principal itself.

This is the point most pre-retirement planning conversations get wrong.

A household past 59½ converting $100,000 in 2026 has immediate access to that $100,000 the day after the conversion clears — with no tax and no penalty on the principal. Conversions of $100,000 in each of the next four years compound that access. By the end of year five, that household has converted $500,000, and every dollar of the original principal is available without restriction at any time during the window.

What the household cannot do during those five years is withdraw more than the $500,000 in cumulative converted principal. Anything pulled out beyond that amount comes out of earnings — and the earnings still owe tax until the 5-year window for each tranche closes.

A simple example: a 62-year-old converts $100,000 today. Tomorrow, she can withdraw the entire $100,000 with no tax and no penalty. Eighteen months later, after the converted balance has grown to $120,000, she withdraws $120,000. The first $100,000 comes out clean; the $20,000 of earnings is taxable income.

This dynamic is one of the reasons Q3’s planning emphasizes that conversion principal stays effectively liquid for households past 59½ — closer to a brokerage account than the locked-up “retirement money” most people assume.

Withdrawing Contributions vs. Earnings — Why It Matters

The 5-year rule does not apply to Roth contributions in the strict sense. Whatever a household has directly contributed to a Roth — money that already had income tax paid on it before going in — can be withdrawn tax-free and penalty-free at any time, regardless of age and regardless of how long the account has been open.

This is the cleanest piece of the rule, and it is worth flagging because the language around the 5-year rule often makes Roth withdrawals sound more restrictive than they actually are. The rule governs earnings and converted balances. Contribution principal is always accessible.

Penalties for Early Withdrawal of Earnings

When a household withdraws earnings before both 5-year-rule conditions are met — both the time requirement and the age 59½ threshold — the IRS treats those earnings as ordinary income. A 10% early withdrawal penalty applies on top, unless one of the qualifying exceptions covers the situation.

The exceptions are narrow. They include disability, qualified first-time home purchase (capped at $10,000 lifetime), certain higher-education expenses, qualified birth or adoption expenses, and inherited Roth accounts. They do not include “I needed the money for a renovation” or “the market dropped and I wanted to rebalance.”

The Counterintuitive Move Most IRA Millionaires Miss

Among the patterns Q3 sees most often in pre-retirement households is the choice to keep funneling new dollars into a Roth IRA or Roth 401(k) contribution year after year — even when the household already holds seven figures in pre-tax retirement assets that will eventually generate forced Required Minimum Distributions.

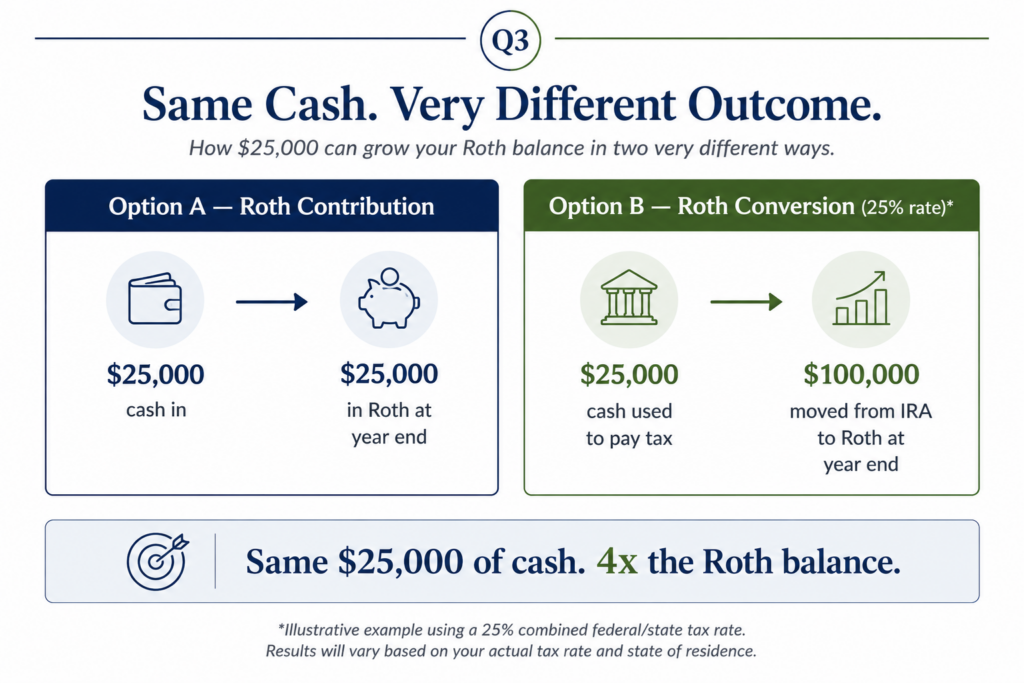

The math frequently rewards a different choice. Consider a household with $25,000 of available cash earmarked for “Roth savings” this year and a household marginal tax rate of roughly 25%. Two options:

- Option A — Contribute $25,000 to a Roth. End of year: $25,000 in the Roth.

- Option B — Use that same $25,000 to pay tax on a $100,000 Roth conversion from an existing IRA. End of year: $100,000 in the Roth.

Both options use the same $25,000 of cash. Option B moves four times as much pre-tax money into the Roth, and that converted balance permanently leaves the pool that will eventually drive RMDs.

The actual tax rate, conversion size, and household-specific cash flow will shift the numbers in any given situation. But the underlying principle holds: for IRA Millionaire households nearing retirement, deliberately accelerating conversions tends to outperform routine Roth contributions on a lifetime tax-adjusted basis. Q3’s article on optimizing retirement income with Roth conversions walks through how the bucket strategy reinforces this.

Why RMDs Drive the Real Math

The reason the contribution-versus-conversion trade-off matters is the Required Minimum Distribution schedule. Starting at age 73 under current law, every dollar inside a Traditional IRA or pre-tax 401(k) begins generating mandatory taxable withdrawals — whether the household needs the money or not.

For a household carrying a $1.5 million IRA into their 70s, those RMDs commonly approach $60,000 a year in the early RMD years and climb steadily as both the balance and the IRS withdrawal divisor age. The income shows up regardless of need, stacks on top of Social Security and pensions, drives IRMAA tier increases, and frequently pushes surviving spouses into single-filer brackets that compound the problem. Q3’s deeper analysis of Roth conversions and RMDs covers the dynamic in detail.

Q3’s average IRA Millionaire client — typically a household with around $1.5 million in pre-tax retirement assets — saves roughly $3 million in lifetime taxes through a properly modeled conversion plan. The savings come almost entirely from collapsing the RMD pile before it fully matures, which means converting larger lumps earlier rather than feeding new contribution dollars into a Roth at the back end.

Common 5-Year Rule Mistakes

- Treating one 5-year rule as covering everything. The contribution clock and conversion clock are separate, and each conversion has its own clock. A single mental “5-year period” misses the structure.

- Thinking conversion principal is locked up before five years are out. Past 59½, converted principal is immediately accessible. The 5-year rule applies only to earnings.

- Letting the rule discourage conversions. The 5-year clock is a planning input, not a barrier. For a household past 59½ with a multi-year conversion plan, the clocks become a non-issue for the principal balance.

- Confusing the contribution clock with the inherited Roth rules. Non-spouse beneficiaries face a separate 10-year withdrawal window under the SECURE Act, which sits alongside — not inside — the 5-year rule.

- Pushing more contribution dollars in instead of converting. For IRA Millionaire households, the counterintuitive move usually wins. Q3’s piece on paying Roth conversion taxes covers how to structure that.

About Q3 Advisors

Q3 Advisors is a flat-fee fiduciary firm specializing in tax-efficient retirement planning for high-income professionals and retirees. As practitioners of Rothology — the science of Roth conversion optimization — Q3 Advisors brings deep expertise in 5-year rule sequencing, multi-year conversion modeling, and lifetime tax-adjusted net worth analysis to help clients navigate complex tax rules and maximize long-term wealth. With $9 billion in projected tax avoidance for clients over more than 14 years, Q3 Advisors has the track record to guide your strategy.

Frequently Asked Questions

What is the 5-year rule for Roth IRAs in plain English?

The 5-year rule is the IRS condition that says earnings inside a Roth IRA can only come out tax-free after the account has been open for five tax years and the owner is at least 59½ (or meets a narrow exception). Direct contribution principal is exempt — it can come out anytime. Converted principal is exempt after 59½, but earnings on converted balances follow the conversion-specific clock.

When does the 5-year clock start?

The clock starts on January 1 of the tax year in which the contribution or conversion is made — not the actual date of the transaction. A conversion completed in December 2026 starts the clock at January 1, 2026, and closes the window on January 1, 2031.

Does every Roth conversion start a new 5-year clock?

Yes. Each conversion year carries its own clock for the converted dollars in that year. A household converting in 2026, 2027, and 2028 has three overlapping clocks, each running independently. Past 59½, this matters only for the earnings on those conversions, not the converted principal.

Can a household past 59½ access converted money immediately?

Yes — for the converted principal. After 59½, conversion principal can be withdrawn at any time without tax or penalty. Only earnings on that converted balance remain subject to the five-year holding requirement. This is the most commonly misunderstood part of the rule.

Can Roth contributions always be withdrawn tax-free?

Yes. Money a household has directly contributed to a Roth IRA — versus money that was converted from a pre-tax account — can be withdrawn at any time, at any age, tax-free and penalty-free. The 5-year rule governs earnings and conversion balances, not contribution principal.

What happens if earnings are withdrawn before the 5-year requirement is met?

Earnings withdrawn before both the time requirement and the 59½ threshold are met are treated as ordinary income, with an additional 10% early withdrawal penalty unless a qualifying exception applies. Exceptions include disability, first-time home purchase up to $10,000, certain medical and higher-education expenses, and qualified birth or adoption expenses.

How does the 5-year rule affect a multi-year Roth conversion plan?

For households past 59½, the rule generally does not interfere with a multi-year conversion plan, because converted principal is immediately accessible regardless of clock status. The rule matters most for households converting before 59½, or for households planning large withdrawals of earnings within a few years of the conversion.

Plan Your Roth Conversion Strategy Today!

Understanding the 5-year rule is the foundation of a working Roth conversion plan — but the sequencing of contributions, conversions, and withdrawals is where the real lifetime tax savings come from. Q3 Advisors models the full lifetime impact of every conversion scenario, with no product pitch and no obligation. Schedule a consultation to see what a properly paced plan looks like for your retirement.