For households that have spent decades building serious retirement wealth — seven-figure balances across traditional IRAs, 401(k)s, and 403(b)s — Roth conversions are no longer an unfamiliar concept. Most IRA Millionaires have at least considered one. Many have run scenarios in spreadsheets. Some have already completed a few partial conversions through their existing advisors. The question is no longer “what is a Roth conversion?” It is “am I doing this in the way that actually maximizes the outcome?”

After more than 14 years and over 2,400 multi-year conversion plans, our team has watched a consistent gap emerge: most households understand the what of Roth conversions, but few fully optimize the how. That gap routinely costs IRA Millionaire households hundreds of thousands of dollars over their lifetime. This article walks through the three optimization steps that separate a decent 2026 conversion from a fully optimized one — start timing, asset selection, and risk allocation — and shows where each step is most often missed.

Why Most Conversion Plans Are Only “Decent”

On paper, a Roth conversion looks simple: move money from a traditional IRA into a Roth IRA, pay the tax on the converted amount at ordinary rates, then let the converted balance grow tax-free for the rest of life. The mechanics are easy to explain in two sentences.

The difference between a “decent” conversion and a fully optimized one rarely lives in the mechanics. It lives in three places the mechanics never address: when the conversion gets executed within the year, which assets get moved first, and how the overall portfolio is rebalanced around the move. Each of those decisions, made well, can produce six-figure savings over a retirement lifetime. Made carelessly, each one produces a meaningfully worse result while everyone involved nods at the same pie chart.

Build a Personalized Conversion Plan

Our team has built more than 2,400 multi-year conversion plans for IRA Millionaire households, and the difference between a generic plan and an optimized one routinely runs into the six and seven figures. Find out what an optimized plan looks like for your situation — with no product pitch and no obligation.

Step 1: Start Earlier Than You Think

The single most common pattern our team sees is the late-year call. October, November, and especially December bring waves of households asking whether a conversion still makes sense this year. We can help — but we’re already behind by the time the call comes.

Roth conversions reward time. Time to model the projected RMD picture. Time to layer in Social Security, pension, or wage income for the year. Time to coordinate with charitable plans. Time to watch how investment performance moves through the year and convert into temporary drawdowns when they happen. Once December 31 closes, the decision is permanent and the year’s strategy is locked.

A 2026 conversion plan really should be drafted in the first quarter of 2026. Starting early opens a wider window for tactical decisions during the year. The first step is usually quantifying the future RMD problem the conversion is designed to solve — our team has built a free RMD calculator that produces a personalized impact estimate in about 30 seconds. From there, the conversion plan can be calibrated to real numbers rather than a year-end approximation. For more on annual timing, see our team’s analysis of the best time of year for a Roth IRA conversion.

Step 2: Convert the Right Assets First

Most of the optimization lives in this step. The question isn’t only how much to convert — it’s what specifically to convert.

A traditional IRA typically holds a mix of asset types. For optimization purposes, those assets fall into three broad groups:

High-growth assets. Equity funds, individual stocks, growth-oriented index funds, certain alternative investments. These are the assets expected to compound the most over the rest of the household’s lifetime.

Medium-growth assets. Balanced funds, dividend-oriented equity, moderate-allocation strategies. Real long-term return but lower expected ceiling than pure growth holdings.

Low-growth assets. Cash, money market positions, short-term bonds, low-yield fixed income. Capital preservation, not capital appreciation.

The optimization rule is straightforward: high-growth assets convert first. Whatever moves into the Roth grows tax-free for the rest of the household’s life, so the assets with the highest expected growth produce the largest tax-free compounding inside the Roth — exactly what makes the conversion worth doing. Cash and short-term bonds inside a Roth still grow tax-free, but the tax-free growth doesn’t amount to much because the underlying return is low.

| Asset Type | Conversion Priority | Reason |

|---|---|---|

| Equity funds, individual stocks, growth ETFs | Convert first | Highest expected tax-free growth |

| Real estate or alternatives inside a self-directed IRA | Convert first (when structure permits) | Often outperforms equities over long periods |

| Temporarily depressed high-quality positions | Convert first while depressed | Tax owed on lower value; recovery is tax-free |

| Balanced funds, dividend equity, moderate allocations | Convert in the middle | Moderate growth, moderate priority |

| Cash, money market, short-term bonds | Convert last or leave | Tax-free growth on low return adds little |

Two specific situations magnify the high-growth-first principle.

Temporarily depressed assets. When a high-quality growth holding is down 10% or 15% from its recent value, converting it while it’s down is a powerful move. The household pays conversion tax on the depressed value. The full recovery — and any additional growth — happens inside the Roth, tax-free forever. For more on conversion timing during volatile markets, see our team’s analysis of navigating Roth conversions in a volatile market.

Real estate inside an IRA. Some households hold direct real estate or real estate partnerships inside a self-directed IRA. These positions often outperform traditional equity holdings over long periods, which makes them strong conversion candidates when the structure permits.

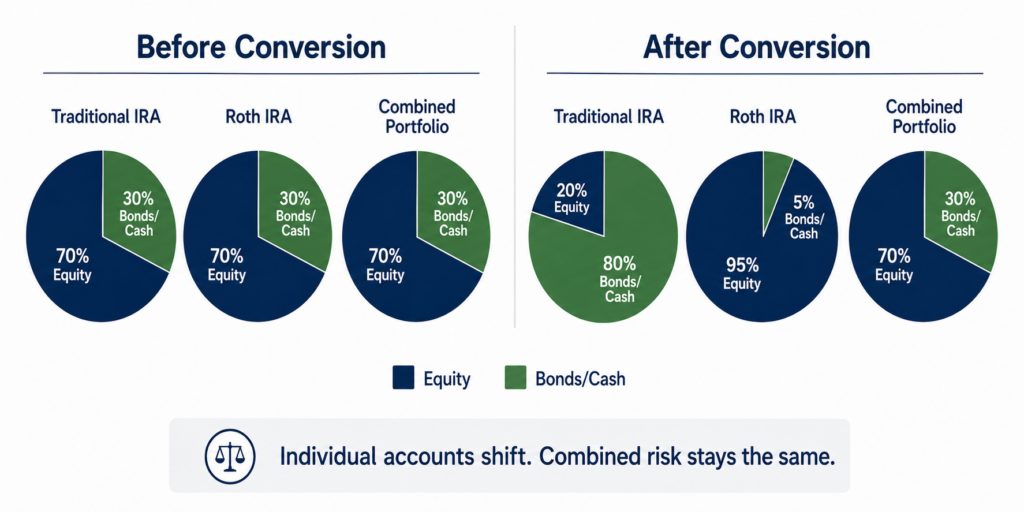

Step 3: Keep Your Overall Risk Allocation the Same

The third step is structural and the most frequently missed.

When a household begins converting, the default move many custodians and advisors recommend is to convert a proportional slice of every holding — keep the new Roth’s allocation mirroring the traditional IRA’s. That looks neat on each individual account’s pie chart. It also defeats the purpose of Step 2.

The correct frame is the combined portfolio. The traditional IRA and the Roth IRA together represent one household balance sheet. After a conversion sequence designed around Step 2, the traditional IRA will look heavier in cash and bonds and lighter in equities. The Roth IRA will look heavier in equities and lighter in cash. Each account, viewed in isolation, will look “unbalanced.”

The combined view doesn’t have to change at all. The household’s overall stock-to-bond ratio, sector exposure, and risk level can remain identical to the pre-conversion picture. The strategy isn’t adding risk — it’s relocating where the growth lives so the growth happens in the tax-free account.

Most assets can be moved this way without selling — a process called an “in-kind” transfer. The same shares, the same positions, simply move from the custodian’s traditional IRA account to its Roth IRA account. No advisor change required. No fund liquidation required. The conversion tax is owed on the value at the moment of transfer, and the position keeps compounding inside the Roth.

A Real Case Study: Susan and John — $1.2M in Tax Savings

To make the optimization difference concrete, consider Susan and John (names changed) — a couple in their mid-60s who came to our team with a substantial seven-figure traditional IRA balance. They had been doing modest annual conversions through their existing advisor, who was applying a proportional approach: convert a slice of every holding each year, keep both accounts balanced individually.

The plan their advisor had built was “decent” by the standard most households measure against. It would have saved real dollars over their lifetime compared to doing nothing.

Our team rebuilt the plan around the three optimization steps. The next conversion year shifted from Q4 into Q1. Equity holdings — including a few positions that had recently pulled back — got sequenced to convert first, while cash and short bonds stayed in the traditional IRA. And the combined-portfolio view got restructured so the new Roth held the bulk of the growth allocation and the remaining traditional IRA held the conservative side, keeping their overall risk profile identical to before.

The projected lifetime tax savings versus the original advisor plan: approximately $1.2 million. Same advisor for investment management. Same custodian. Same overall risk level. Same retirement lifestyle. The optimization produced the entire difference. For more on the planning approach behind outcomes like this, see strategic Roth conversions that save over $1 million in taxes.

Common Mistakes to Avoid

Several errors quietly compound the cost of an under-optimized conversion plan:

- Calling in October or later. A conversion plan built in Q4 has a fraction of the planning surface area of one started in Q1. The compressed timeline removes optionality.

- Converting proportionally instead of by asset type. Moving “a little bit of everything” keeps individual pie charts tidy and leaves the bulk of optimization unrealized.

- Selling positions to convert them. Most positions can move in-kind. Selling first creates unnecessary friction and, in taxable accounts, unnecessary capital gains.

- Confusing combined risk with account-level risk. The traditional IRA and Roth IRA should be viewed together. Each account’s allocation can shift dramatically while the household’s combined allocation stays unchanged.

- Treating the conversion as a one-time event. Most optimized plans run four to ten years. Each year recalibrates to current income, balances, and tax-law context. For more, see our team’s analysis of multi-year Roth conversion strategies.

For a broader look at the planning errors that derail conversion strategies, see 5 costly Roth conversion mistakes.

About Q3 Advisors

Q3 Advisors is a flat-fee fiduciary firm specializing in tax-efficient retirement planning for high-income professionals and retirees. As practitioners of Rothology® — the science of Roth conversion optimization — our team brings deep expertise in the timing, asset sequencing, and combined-portfolio thinking that separates a decent conversion from a fully optimized one. We don’t sell financial products and we don’t manage investment accounts — we sit on top of what households already have and help them make smarter decisions about how and when to move their money. With $9 billion in projected tax avoidance for our clients over more than 14 years, we have the track record to guide your strategy.

Frequently Asked Questions

When should I start planning my 2026 Roth conversion?

As early in 2026 as practical. The first quarter offers the widest planning window, the most flexibility to react to market movements during the year, and the most time to coordinate the conversion with other tax events. December-only conversions still get done, but the compressed timeline costs optionality and forces tactical decisions to be made under time pressure.

Which assets should I convert first?

In most cases, the highest-growth assets in the traditional IRA. Whatever moves into the Roth grows tax-free for the rest of the household’s life, so the assets with the largest expected growth produce the largest tax-free compounding. Cash, money market positions, and short-term bonds typically convert last — tax-free growth doesn’t add much value to low-return holdings.

Won’t converting growth assets first make my Roth riskier than my IRA?

The individual account allocations will shift, yes. The combined-portfolio allocation does not have to change at all. If the household held 70% equities and 30% bonds before the conversion, the combined IRA and Roth can still hold 70% equities and 30% bonds after — just with the equities living predominantly in the Roth and the bonds living predominantly in the traditional IRA.

What is an “in-kind” transfer?

An in-kind transfer moves shares or positions from one account to another without selling them. A position that held 200 shares of an ETF in the traditional IRA on Monday holds the same 200 shares in the Roth IRA on Tuesday — no sale, no liquidation, no fund change. The conversion tax is owed on the value at the moment of transfer, but the position itself continues uninterrupted.

Can I do this through my existing financial advisor?

Often yes, particularly for the mechanics of executing transfers. The harder part is the optimization layer — modeling lifetime projections, sequencing assets across multiple years, coordinating with Social Security and IRMAA thresholds. Many general-practice advisors don’t have the tools or specialization for that work. The conversion plan and the investment management can sit with different professionals without conflict.

How is “fully optimized” different from just “doing a Roth conversion”?

A standard Roth conversion captures most of the basic tax-free-growth benefit. A fully optimized conversion captures additional savings through the three steps in this article — start timing, asset sequencing, and combined-portfolio risk management — plus multi-year sequencing, IRMAA threshold management, survivor-bracket modeling, and integration with charitable and estate plans. For a seven-figure IRA, “fully optimized” routinely produces six- or seven-figure lifetime savings beyond “decent.”

Plan Your Roth Conversion Strategy Today!

The difference between a decent Roth conversion and a fully optimized one routinely runs into the six and seven figures for IRA Millionaire households — and the three optimization steps above are where most of that difference lives. To find out what a fully optimized 2026 plan looks like for your specific situation, schedule a consultation with our team and get a multi-year projection built around your numbers.